Stretch Hood Film Cost Per Pound in 2026. Ranges, Drivers, and Where the Market Is Heading.

Most film suppliers will not give you a straight answer on price. Here is the breakdown they do not want you to have.

Why is film pricing so opaque?

Ask three film suppliers what stretch hood film costs per pound, and you will get three different answers. None of them will look like a public price.

There is a reason. Film pricing is built from a stack of variables that change weekly. Resin cost, conversion margin, format size, additives, contract structure, and freight. Suppliers prefer to quote a final number rather than show the components, because the components are where the negotiation happens.

That works for the supplier. It does not work for a plant manager trying to budget a packaging line for the next 12 months.

This article opens the black box. Real ranges, what drives each component, and where the market is heading after the Iran war disruption.

What is the actual cost-per-pound range for stretch hood film in 2026?

The honest answer is a range, not a number. The range depends on three primary variables. Format size, film structure, and contract type.

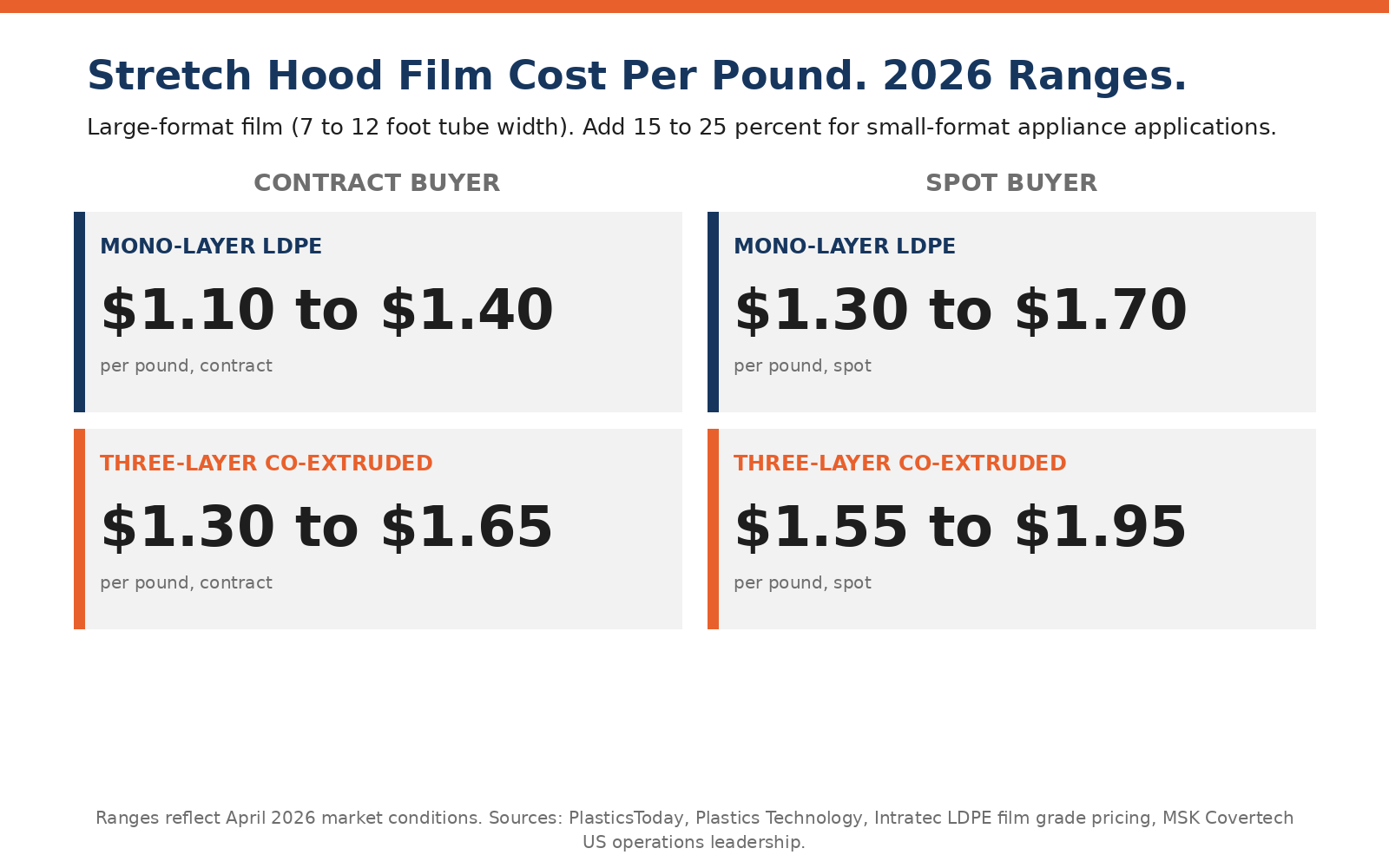

For large-format stretch hood film (7 to 12 foot tube width, used in roofing, building materials, cement, paper, and most industrial applications), current cost-per-pound runs in these approximate ranges.

Mono-layer LDPE film. $1.10 to $1.40 per pound for contract buyers. $1.30 to $1.70 per pound for spot buyers.

Three-layer co-extruded film. $1.30 to $1.65 per pound for contract buyers. $1.55 to $1.95 per pound for spot buyers.

For small-format film (used in appliance and consumer goods packaging), pricing runs higher because the supplier landscape is thinner and most film is imported. Add roughly 15 to 25 percent to the large-format ranges.

These ranges have moved up significantly since February 2026. According to industry reporting from PlasticsToday and Plastics Technology, North American polyethylene contract prices rose roughly 20 cents per pound between March and April 2026, and film extruders have passed those increases through.

What drives film pricing up?

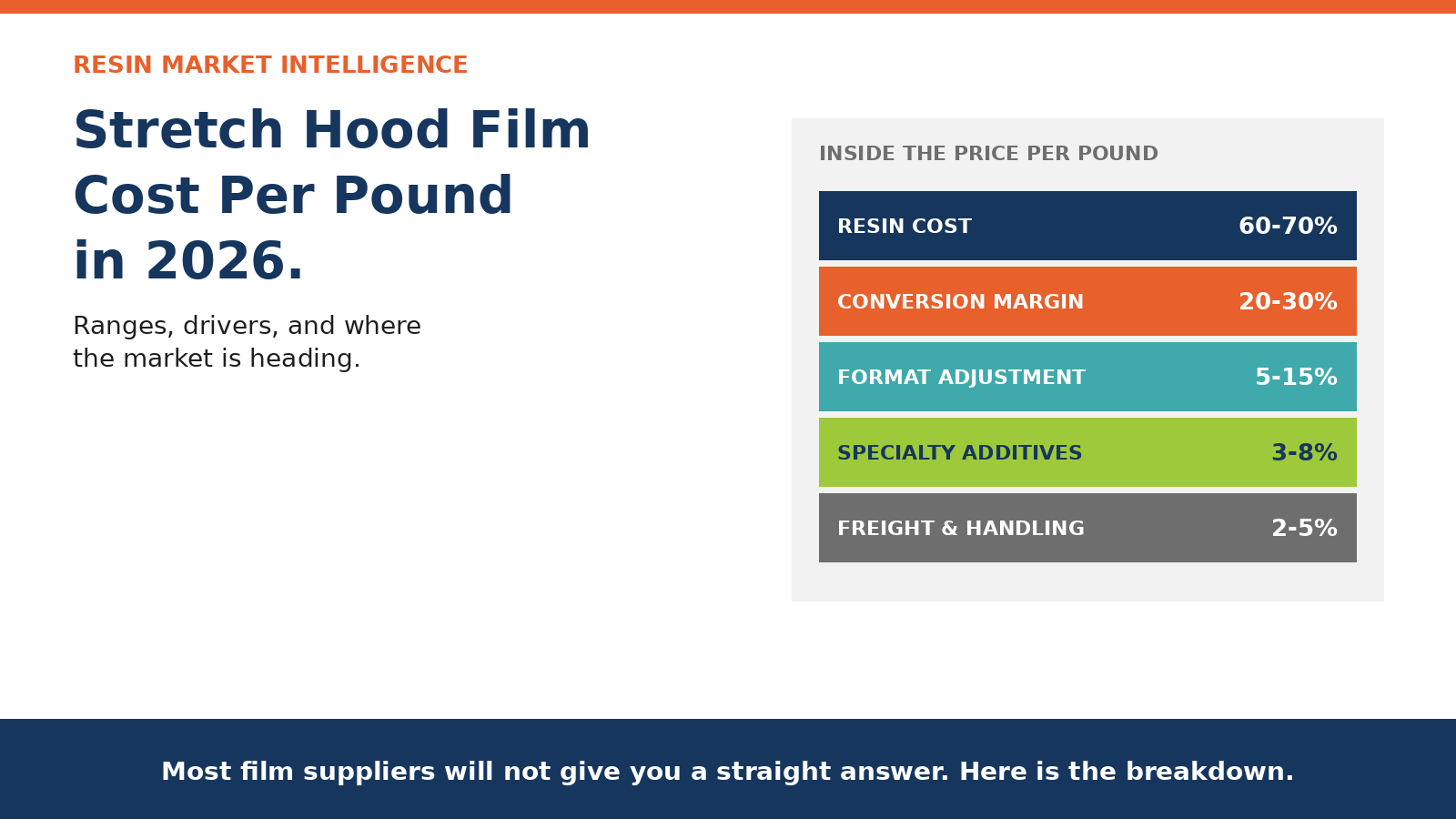

Five components. Each one moves independently.

The resin cost is the largest single input. LDPE film grade resin in the United States traded at roughly 57 cents per pound through most of 2025. By April 2026, that number was in the 70s and still climbing. Resin alone accounts for roughly 60 to 70 percent of finished film cost on a typical mono-layer spec.

The conversion margin is what the film extruder charges to convert resin into film. This typically runs 20 to 35 cents per pound, depending on volume, format, and equipment utilization. Larger and more complex specs cost more to convert.

The format size adjustment runs an additional cost on small-format film. Most domestic extruders lack the small-die capability, which means small-format pricing carries an import premium or a specialty surcharge.

Specialty additives include UV stabilizers, anti-static, and recycled content. Each one adds 3 to 8 cents per pound, depending on the percentage and type.

Freight and handling are typically modest in good markets, but shipping disruption events (like the current Strait of Hormuz situation) can add unexpected cost.

A breakdown showing the five components of stretch hood film pricing stacked from resin cost up through specialty additives and freight.

What drives film pricing down?

Four levers, all of which are inside the buyer's control to some degree.

Scale is the most obvious. Annual commitments above 500,000 pounds typically unlock contract pricing 10 to 20 percent below spot. Above 2 million pounds, the discount widens further.

Multi-year contracts with volume commitments lock in pricing against market volatility. In the current environment, this is the single highest-leverage move a buyer can make.

Domestic sourcing reduces freight, tariff exposure, and currency risk. North American capacity is running above 90 percent utilization right now, which compresses some of the domestic discount, but the structural advantage remains.

Specification discipline is the lever most plant managers underuse. A correctly specified thinner film, run on equipment that is dialed in, can reduce cost per pallet by 15 to 30 percent without any change in supplier or contract structure. This is the downgauging conversation, and it is covered in detail in a companion article.

Where is the market heading?

Three things are reasonably predictable through the rest of 2026 and into 2027.

First, North American resin producers will continue to capture share from the disrupted Middle East and Asian supply. According to ICIS analysis, Middle East petrochemical export recovery is expected to take 12 to 18 months even after the Strait of Hormuz reopens. North American producers are running at peak utilization and are unlikely to add significant capacity in the short term.

Second, contract pricing will remain elevated relative to 2024 and 2025 baselines. Even if the conflict de-escalates, the new floor is higher than the old floor. Buyers signing 2027 contracts at 2024 reference prices are not seeing the current market.

Third, the format size advantage will tilt toward suppliers with diversified production capability. Suppliers that can serve both large-format and small-format buyers will have leverage. Single-format suppliers will see margin compression.

How should a buyer approach a 2027 contract conversation?

Five questions to bring to the table.

What is the resin pass-through structure? Some contracts pass through resin movement automatically. Others lock in for 6 or 12 months. The right answer depends on the buyer's view of the resin market, but the question must be asked.

What are the volume tiers, and how are they calculated? Calendar year, contract year, rolling 12-month, and minimum monthly draw all behave differently. The tier structure is often more negotiable than the headline price.

What is the conversion margin, and how is it documented? Asking for the conversion margin separately is the single most useful negotiation move. Most suppliers will not break it out without being asked. Once it is broken out, it can be benchmarked.

What is the supplier's resin sourcing? Suppliers with diversified resin sources are more resilient to disruption. Single-source resin buyers may offer lower headline prices but carry higher continuity risk.

What is the exit clause? Multi-year contracts should include performance clauses, force majeure language, and reasonable exit rights. A contract with no exit is not a contract; it is a hostage situation.

Why is MSK in this conversation if MSK does not sell film?

This is the part that confuses some buyers at first.

MSK does not sell stretch hood film. MSK manufactures the equipment that runs the film. That distinction matters because it means MSK has no margin interest in any specific film supplier.

According to MSK Covertech's documented installation history, MSK equipment runs across roofing, building materials, cement, paper, flooring, appliance, and distribution categories, which means MSK sees film performance, pricing, and supplier behavior across the entire North American market.

The honest version. MSK is the equipment-neutral expert in a conversation where almost every other voice has a margin position. Film suppliers want to sell film. Brokers want commissions. Consultants want billable hours. MSK wants the equipment to run well, which means the film has to run well, which means the buyer has to be matched with the right supplier at the right spec.

That is the position MSK has built across 6,500 installations worldwide.

When is MSK the right call for this conversation?

If you have a stretch hood line and you have not benchmarked your current film pricing in the last 24 months, this is a useful 30-minute conversation.

If you are signing or renewing a multi-year contract in the next 6 months, the conversation is worth having before signature, not after.

If you are running a competitor brand of equipment, the conversation still applies. The film market and the supplier landscape are the same regardless of who built the machine.

If you do not have a stretch hood line, the conversation is upstream of where you are. The film question comes after the equipment question.

FAQ

Why is small-format film so much more expensive than large-format?

Small-format film (used in appliance and consumer goods packaging) requires small-die extrusion capability that most domestic producers do not have. Most small-format film is imported from Europe, which adds freight, currency, and tariff exposure. There are only two domestic producers with reliable small-format capability at the volumes North American appliance makers consume. Limited supply plus higher input costs equals a premium of roughly 15 to 25 percent over comparable large-format pricing.

Should I lock in a multi-year contract now or wait for prices to come down?

The honest answer depends on the buyer's risk tolerance and view of the market. The case for locking in now is that contract pricing is elevated but stable, and the alternative (spot buying through a continued disruption) carries higher upside risk. The case for waiting is that if the conflict de-escalates faster than ICIS projects, prices may come down. Most buyers split the difference with a 12 to 18-month contract that captures stability without committing to a full multi-year cycle at peak prices.

How much can recycled content reduce or increase film cost?

Post-consumer recycled (PCR) content typically adds 5 to 12 cents per pound at 30 percent loading, depending on the recycled material source and quality. The premium is partially offset by sustainability mandate compliance value for brands with ESG commitments. For pure cost optimization, PCR is not currently the move. For brands with stated sustainability targets, the math changes.

Is there a difference between the stretch hood film cost and the stretch wrap film cost per pound?

Stretch hood film is generally more expensive per pound than stretch wrap film because the formulation requirements are different. Stretch hood film must recover after stretching, which requires specific resin grades and often three-layer co-extrusion. Stretch wrap film is simpler. The per-pound comparison is not the right metric, though. Stretch hood film at $1.40 per pound covers roughly 1,000 pallets per reel, while stretch wrap film at $1.10 per pound covers 150 to 200 pallets per reel. The cost-per-pallet math is what matters, and stretch hood typically wins on that math by a wide margin.

What if my supplier refuses to break out the conversion margin?

That is information. A supplier that will not break out the margin is signaling that the margin is the part of the conversation they would prefer to avoid. The buyer can either accept the bundled price (which is sometimes the right move on small accounts) or escalate the conversation, get a competing quote, or bring in an outside perspective. MSK is one such outside perspective for buyers running stretch hood lines.

The bottom line

Film pricing is opaque because suppliers prefer to quote final numbers rather than show components. The components are where the leverage lives.

Current cost-per-pound for large-format stretch hood film runs $1.10 to $1.95, depending on structure, contract type, and supplier. Small-format runs 15 to 25 percent higher. The market floor has shifted up since February 2026 and is unlikely to return to 2024 and 2025 reference prices anytime soon.

Five questions to bring to a 2027 contract conversation. Resin pass-through, volume tiers, conversion margin, supplier resin sourcing, and exit clause. None of these is optional.

A 30-minute conversation with someone who has no margin position in your film supplier relationship is worth having before you sign anything.

Reporting and analysis prepared for MSK Covertech. MSK Covertech is a German-owned manufacturer of stretch hood and shrink hood end-of-line packaging equipment, founded in 1975, with over 6,500 systems installed worldwide and US operations led by Braden Camp out of Acworth, Georgia.

SOURCES REFERENCED: PlasticsToday (resin pricing reports, March-April 2026), Plastics Technology (April 2026 resin price column), ICIS (Strait of Hormuz recovery analysis, April 2026), Intratec (LDPE and LLDPE price assessments), Plastics News (resin price tracking), MSK Covertech US operations leadership.

Ready to find your packaging partner?

Join hundreds of manufacturers and buyers already using PackageLink to streamline their sourcing process.