The Margin Expansion Lever Your Portfolio Company's Management Is Hiding From You.

This is not a marketing pitch. This is not a technology solution. This is not a rebranding exercise.

This is a direct conversation with private equity operating partners and board members who have acquired packaging distribution businesses, applied the standard operational playbook... cost reduction, procurement optimization, CRM implementation, sales force expansion and are watching the margin compression continue anyway.

You are not getting the returns you underwrote. The hold period is extending. And when you ask the portfolio company's leadership why the business isn't growing faster,you are getting some version of the same answer: it's a tough market, our reps are working hard, we're investing in marketing, we're building the website.

They are not lying to you. They genuinely believe those things. But they are describing symptoms as if they were strategies. And nobody in the building, including your operating partner who visits quarterly has identified the actual problem.

The actual problem is that your packaging distribution business is competing in a commodity market it cannot win. And the solution, a documented, executable, margin-expanding specialty niche strategy is being dismissed by portfolio company leadership as something vague and soft and not-really-their-job.

They call it "marketing." They call it "an IT thing." They say the reps "already do this." And then they go back to quoting stretch wrap at fractions of a penny and wondering why the numbers aren't moving.

01 WHAT YOU'RE ACTUALLY SITTING ON

Let's start with the financial reality, because that's the language that matters in thisconversation.

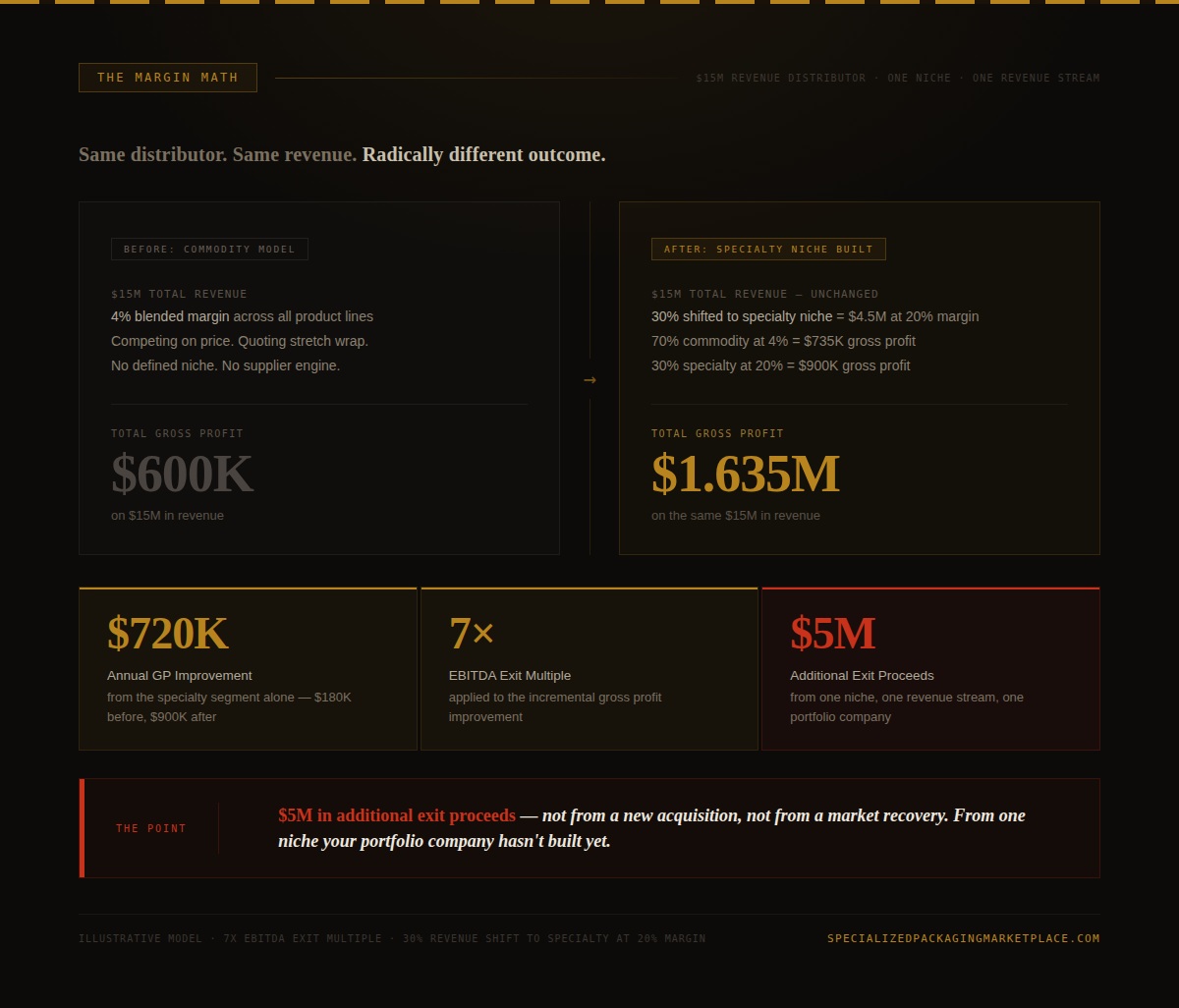

Commodity packaging distribution...stretch wrap, corrugated boxes, poly mailers, basic void fill...generates margins of 2 to 4 cents per dollar of revenue before overhead and delivery costs. This is not a cyclical compression. This is a permanent structural condition created by Uline's next-day shipping, Grainger's 1.5 million SKU catalog, and Amazon Business undercutting your distributor's quote while the rep is still on the phone.

Specialty packaging distribution, technically differentiated niches like flexible aseptic packaging, EPR-compliant sustainable films, or validated cold-chain solutions, generates margins of 15 to 28 cents per dollar. With customers who have genuine switching costs. With supplier relationships that create supply chain advantages competitors cannot replicate. With reps who are having consultative conversations instead of quoting races.

Now answer this question honestly: does your packaging distribution portfolio company have a documented specialty niche strategy? Not a tagline on the website. Not a product category they "focus on." A real, operational, Win Program with a defined target customer, a specific Pain Map, direct supplier relationships, trained reps, and a measurable win condition?

If the answer is no, and for the overwhelming majority of PE-backed packaging distributors,the answer is no, then you are operating a commodity business inside a PE ownership structure that is paying commodity multiples and hoping for specialty returns. That math does not work.

02 WHY YOUR PORTFOLIO COMPANY'S LEADERSHIP ISN'T FIXING THIS

Here is what you need to understand about the leadership team at your packaging distribution portfolio company, and I am going to say this with the directness the situation deserves:

They built their careers in the commodity model. They are good at the commodity model. And they are deeply, almost viscerally, resistant to the idea that the commodity model is structurally broken.

When you tell them their reps need to sell differently, they hear an accusation. When you tell them they need a specialty niche, they hear an implication that everything they've built was wrong. When you bring in outside expertise to help them identify a high-margin opportunity, they label it "marketing" or"IT" or "that consultant thing" and then they wait for it to go away.

This is not incompetence. This is human nature. It is also the single most common reason PE value creation plans in distribution businesses fail to produce the EBITDA improvements they were designed to deliver.

Portfolio company resistance is not a personnel problem you solve by replacing the CEO. It is a structural problem you solve by changing what gets measured, what gets rewarded, and what gets escalated to the board when it doesn't happen.

The research on this is unambiguous. A survey of PE operating partners across more than 50 major firms found that portfolio company resistance defined as lack of alignment or buy-in at the management level is the single largest obstacle to operational value creation, cited in 35% of underperforming initiatives. In industrial distribution specifically, where workforces are long-tenured and processes are analog, the resistance is structural rather than individual.

The answer is not to hire new leadership and hope the new team figures it out. The answer is to install a documented program with defined metrics, external accountability, and board-level visibility that makes resistance the more difficult path.

03 THE LEVER YOU HAVEN'T PULLED

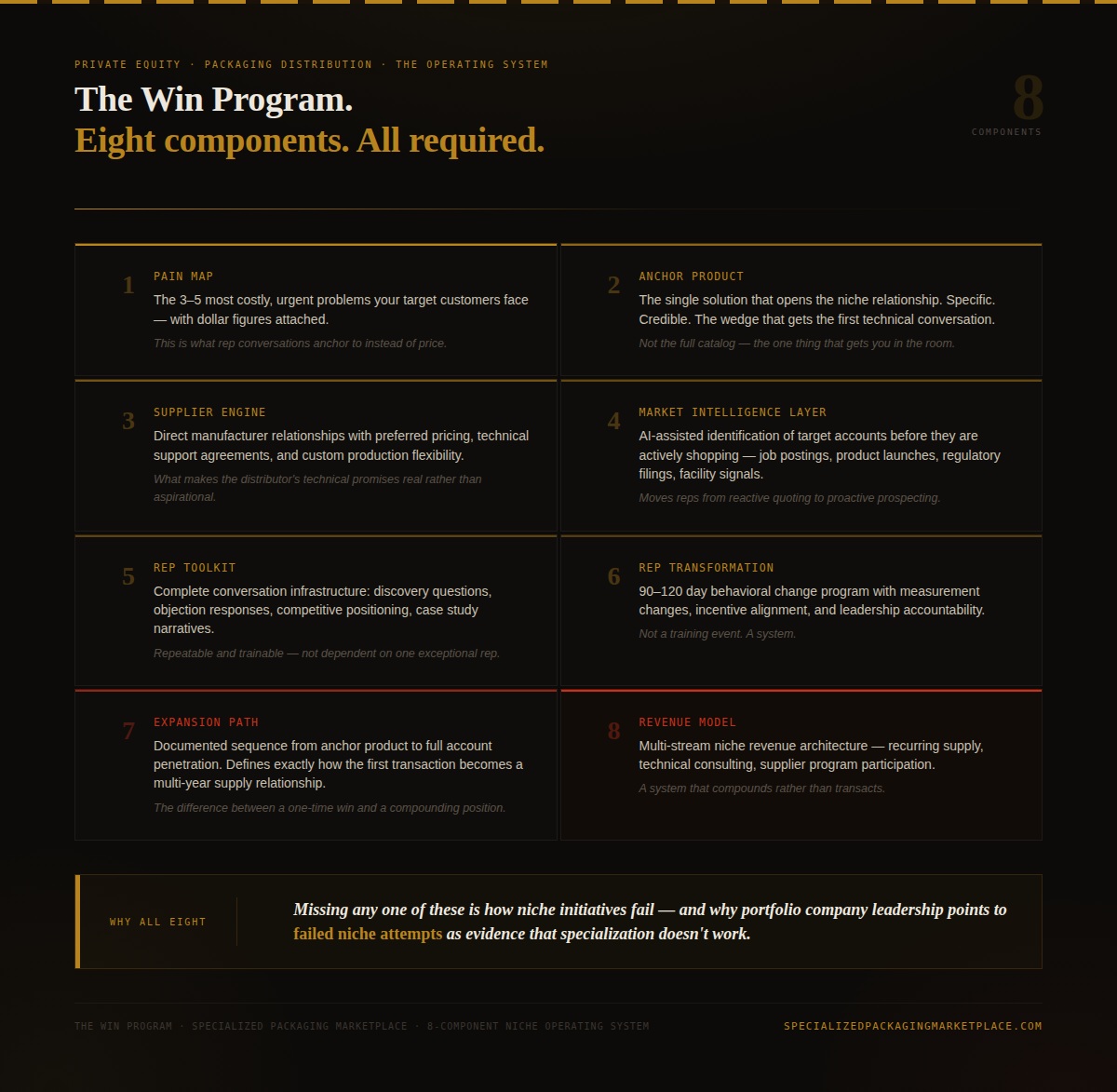

The Win Program is a documented, eight-component operational framework for transforming a commodity packaging distributor into a specialty category owner. It is not a consulting engagement. It is not a training seminar. It is a complete operating system built for packaging distribution specifically that moves margin from 3 cents per dollar to 18–25 cents per dollar within 12 months on the niche revenue stream.

It has eight components because all eight are required. Missing any one of them is how niche initiatives fail and why portfolio company leadership points to failed niche attempts as evidence that specialization "doesn't work." It doesn't work when it's half-built. It works exceptionally well when all eight components are operational.

04 WHAT PE FIRMS ARE GETTING WRONG IN THEIR DILIGENCE

Private equity firms evaluating packaging distribution acquisitions are doing thorough financial diligence. They are stress-testing revenue concentration, analyzing customer churn, modeling working capital cycles, and pressure-testing margin assumptions. This is the right work. It is also incomplete.

What is missing from the diligence process in almost every packaging distribution acquisition I have observed is a rigorous assessment of specialty niche potential: the question of whether this business has the customer base, the rep talent, and the market position to build a defensible specialty revenue stream that the commodity analysis doesn't capture.

The reason this is missing is that nobody on the deal team knows to look for it. Investment bankers present the business as it currently operates a commodity distributor with X accounts and Y margin. Operating partners stress-test whether the commodity margins can be maintained or slightly improved. And the specialty niche opportunity which is almost always visible in the profitable customer data and the domain knowledge of specific reps goes unexamined.

That is a diligence gap that costs PE firms multiple points of EBITDA over the hold period.

EY research on PE value creation in wholesale distribution identifies specialty positioning explicitly as a source of sustainable advantage noting that specialty distributors hold stable, attractive roles in B2B value chains and command premium multiples precisely because their customer relationships are not replicable by commodity platforms. The opportunity is documented. The framework exists. The gap is in knowing where to look and how to build it.

The most valuable niche opportunity in your packaging distribution portfolio company almost certainly already exists inside the business. It is invisible because nobody has done the discovery work to find it and nobody in management has been given the mandate to build it.

05 THE THREE CONVERSATIONS YOU NEED TO HAVE THIS QUARTER

Conversation One: The Profitability Audit.

Pull your portfolio company's customer data sorted by margin per transaction not revenue. Find the top 20% of accounts by profitability. Ask management: why do these specific customers stay, and what would it cost them to leave? If management cannot answer that question specifically, that is diagnostic. It means they do not understand the value they are already providing and they have no strategy for replicating it.

Conversation Two: The Sales Behavior Audit.

Ask your operating partner to ride along on ten rep calls not a review of call logs, actual conversations. Count how many of those conversations involve a rep diagnosing a customer's problem versus quoting a price. If the answer is fewer than two out of ten, your reps are order takers in a commodity business. That is not a personnel problem. It is a system problem that requires a Win Program to fix.

Conversation Three: The Niche Discovery Conversation.

Bring in an outside assessment specifically structured around the five-step niche discovery framework that examines your specific portfolio company's customer base, competitive landscape, rep talent, and supplier relationships to identify the highest-probability specialty niche opportunity. This is a paid engagement, not a free pitch. It produces a documented recommendation or an honest assessment that conditions are not right. Either outcome informs your value creation plan.

06 WHO WE ARE AND WHY THIS CONVERSATION

The Specialized Packaging Marketplace was built by David Marinac 35 years inpackaging manufacturing, distribution, and business development specifically to address the gap between where packaging distribution businesses are and where they could be with a correctly executed specialty niche strategy.

The Marketplace provides three things that PE-backed packaging distributors need and currently lack: a documented Win Program framework built specifically for packaging distribution, direct access to specialty packaging manufacturers with the technical depth and production flexibility to support niche programs, and an AI-driven market intelligence capability that identifies target accounts before they are actively shopping.

We work with packaging distributor ownership, PE operating partners, and board members who are serious about building specialty positions not dabbling in them. The engagement model is structured and paid. We do not do free strategy sessions. We do not produce 80-page consulting reports that get filed. We build operational programs that move EBITDA.

The whitepaper behind this letter "Niche or Die: How Packaging Distributors Escape the Commodity Trap and Become Category Killers" is available on request and provides the complete strategic and operational framework referenced here.

The Direct Question.

You acquired a packaging distribution business because you saw value creation potential. You were right it's there. But it is not in the commodity revenue stream your team has been optimizing. It is in the specialty niche that nobody in the portfolio company has built, because nobody gave them the framework, the mandate, or the accountability structure to build it.

The margin is sitting there. The customer relationships that anchor it already exist in your portfolio company's data. The rep talent that can execute it is probably already on the payroll.

The only thing missing is the decision to build it and the program that makes the decision real.

That is the conversation we are here to have.

Ready to find your packaging partner?

Join hundreds of manufacturers and buyers already using PackageLink to streamline their sourcing process.